Scheme funding in volatile conditions: TPR’s 2016 annual funding statement

Elizabeth Wise contributed to the writing of this blog post.

Schemes undertaking funding valuations often face a valuation-date lottery. According to The Pensions Regulator’s (TPR’s) 2016 funding statement, this year is no different.

"The statement highlights the importance of taking an integrated approach to funding, investment and covenant as set out in their recent guidance."

TPR’s statement is intended to help trustees navigate the challenging waters of relatively volatile market conditions, and illustrates a marked difference in how much funding positions can change between valuations, depending on the dates in question.

For example, if the valuation is carried out at the end of March 2016, it is likely to show a worse position than if the valuation date was three months earlier. TPR expects the increase in deficits since the previous valuation date could be “in the region of 20-35%, depending on the scheme’s valuation date and hedging strategy”.

The statement highlights the importance of taking an integrated approach to funding, investment and covenant as set out in their recent guidance. In this blog, the first of a series of three, we consider TPR’s key messages concerning investment.

Asset returns generally good…

Assets have generally performed well over the period although, as can be seen in the chart below, investment markets have exhibited significant volatility.

This is particularly the case for UK equities. Over the three year period to 31 December 2015, investing in the FTSE All Share Index alone would have returned around 23%, whereas over the three year period to 31 March 2016, the return was less than half of this (at 11%).

Index-linked gilts would have returned around 21% over the three years to 31 December 2015, and around 18% over the three years to 31 March 2016.

As a result, valuations as at 31 March 2016 may show a smaller improvement in funding level on average than those at 31 December 2015, when considering the impact of market movements alone. Of course, the actual returns on investments for an individual scheme will depend heavily on the scheme’s asset allocation, and investment experience will one of several variables affecting schemes’ funding level progression between valuations.

This highlights the importance of considering investment strategy alongside funding strategy.

Total returns for a range of asset classes since March 2010

Sources: The Pensions Regulator, Thomson Reuters

TPR states that trustees should not be overly focused on short-term market movements, but it is important that they understand how this volatility will impact on their views of future investment returns and risks. This will then feed into the trustees’ funding plans.

As ever, trustees should consider making an allowance for post-valuation experience when setting their recovery plans, particularly when markets have been volatile.

…but outweighed by increasing liabilities

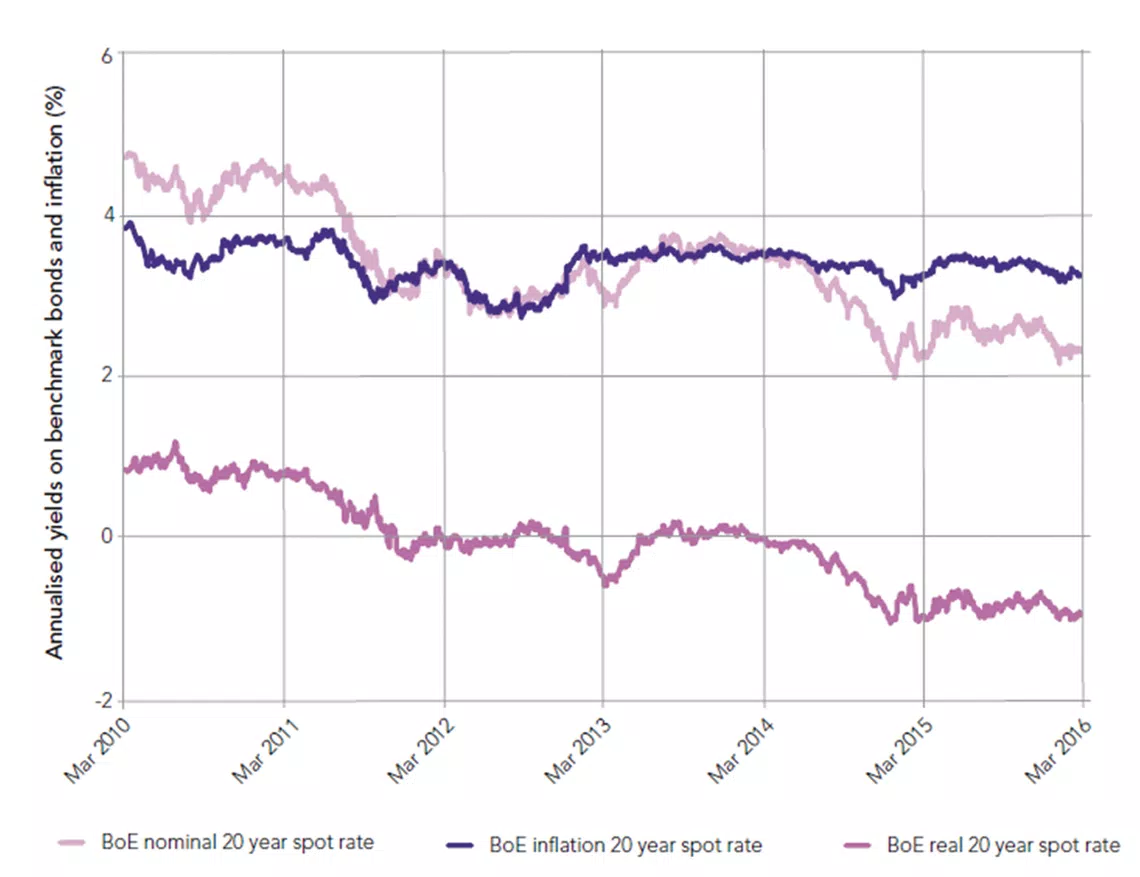

Market yields on government bonds are key indicators used to set assumptions for future investment returns – particularly as they are indicative of the market’s view of a (relatively) ‘risk-free’ rate of return. There was a significant fall in gilt yields towards the end of 2014, and the position has not significantly improved since then. As a result TPR expects that, all else being equal, schemes will use lower asset return assumptions than their previous valuation.

This will lead to a higher value being placed on the liabilities – and TPR says this increase should more than offset the positive returns on assets for most schemes. Schemes that were previously in deficit and have a higher mismatch between their assets and liabilities will be worst affected.

Gilt yields and implied inflation since March 2010

Sources: The Pensions Regulator, Bank of England, Thomson Reuters

Selecting a single investment return assumption for future years is not the whole picture. Trustees need to take into account the liability profile of their scheme, and make sure that the funding strategy anticipates future changes to investment strategy as the scheme matures, which may include using term-dependent interest rates to discount liability cashflows.

Reconsider yield reversion

Some trustees made an explicit allowance at their last funding valuation for gilt yields to ‘revert’ back from historic low levels to what they viewed as more ‘normal’ levels. That reversion hasn’t happened and TPR makes it clear that trustees who made such an allowance should now “consider implementing the contingency plan that was put in place to manage the impact of these assumptions not being borne out.”

Furthermore, whilst TPR does not rule out the possibility of yields reverting to higher levels at some point in the future, the regulator explicitly spells out that trustees who continue to allow for reversion should “reconsider their assumptions in light of market developments” and may find it necessary to assume reversion “over a longer time period and to lower levels than before”.

"Assets have generally performed well over the period although investment markets have exhibited significant volatility."

Cashflow planning can be critical

Very mature schemes face a further issue. If benefits being paid out are more than contributions being paid in, the scheme will need to sell assets to pay pensions. If the scheme is forced to sell when markets are low, then the funding of the scheme will suffer as a result.

The volatility of returns can therefore have a significant impact on the ability of a scheme to reach full funding – potentially resulting in further contributions being required from the sponsoring employer. Trustees should consider the cashflow needs of their scheme and put plans in place if this could become an issue.

As schemes mature, trustees will need to consider their funding and investment strategies as part of their IRM framework, and TPR suggests they may want to review whether chosen asset allocations are likely to generate suitable free cashflow in future.

This is the first time TPR has explicitly commented on cashflow matters in its annual funding statement.

Our next blog on TPR’s funding statement will look at how trustees can begin to approach funding in the current environment, followed by a look at how TPR’s view on employers’ financial strength has developed. TPR’s recent focus has been on how the three strands of risk management – ie funding, investment and covenant - should be considered as part of an integrated strategy.