Mutuality and with-profits funds: Statements released by the FCA and PRA

Ciara Russell contributed to the writing of this blog post

On 28 March 2014, the FCA and PRA each issued a statement on mutual with-profits life assurance providers. The statements follow Consultation Paper 12/38: 'Mutuality and with-profits funds: a way forward' published late 2012 and have been welcomed by the mutual sector. They are relevant for all mutual insurance firms and friendly societies with books of with-profits business.

The issue of declining with-profits business and the impact this has on the mutual sector is a long running issue for the market. Current rules require a mutual to close to new business when their with-profits business enters run-off, in order to be fair to the members. However, the market has expressed desire for more flexibility and argued that closure is not always in the members’ best interests.

Summary of proposal:

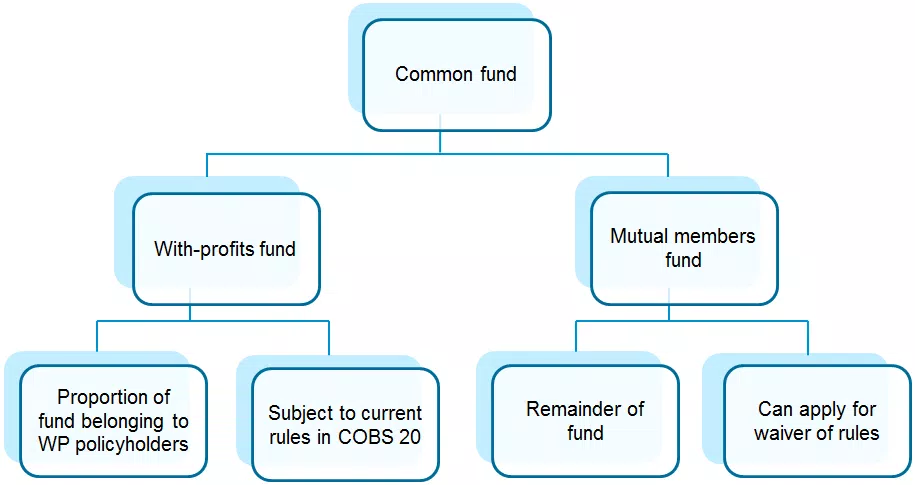

The overall aim of the consultation was to respond to the market’s wishes and to provide mutuals with flexibility. The proposal would allow mutuals to continue writing new without profits business even when the with-profits business has entered run-off by recognising both types of business in a single fund as follows:

New without profits business would be written into the mutual members fund. For mutuals to use this structure, they would need to apply for the waiver of the rules from the FCA and PRA.

The regulators’ statements confirm that the proposal in CP 12/38 will proceed. They address responses to the consultation and provide clarity and detail. Key points are summarised below.

Information provided in the regulators’ statements

Principles to meet

There are various principles to meet in order to be granted a waiver. These are unchanged from the consultation paper although the statements provide clarity on these.

One principle is to provide a convincing and robust business plan. The papers confirm this should be a medium term plan, demonstrating the sustainability of products and using realistic estimates of business volumes and profits.

Another principle is to demonstrate that policyholders in a mutual are no worse off than equivalent policyholders in a proprietary. The FCA recognises this is difficult to quantify and will discuss the practicality of this on an individual basis. Something they can consider is how the size of a policyholder’s inherited estate compares between a mutual and in a proprietary, where product features are very similar. Another comparison might be how costs differ between the two.

One of the principles requires being able to demonstrate that the current unmodified rules are burdensome. Meeting this principle may be difficult for with-profits mutuals that are not in run off and able to write a sizeable amount of with-profits business under the current rule structure. This proposal is available to them should they meet the principles and, as for mutuals, with declining with-profits business, their application will be considered on an individual basis.

Independent expert

All mutuals, including the smallest, are required to obtain an independent expert to review the proposed allocation of funds. The FCA will be involved in the agreement of the independent expert’s terms of reference. Their role includes ensuring that proper consideration is given to the interests of with-profits policyholders.

The FCA stresses the importance of independence of the role so that actions are fair and balanced. The expert cannot become a member or policyholder advocate. The statement implies that a mutuals’ actuarial function holder or with-profits actuary would not provide sufficient independence in the expert role. The FCA will review the level of independence.

The role is not limited to the approved skilled person provider list. The chosen expert will need to have appropriate skills and expertise and probably be an actuary or a similarly qualified person.

With-profits policyholders’ rights and legal advice

Legal uncertainty exists and is acknowledged in the proposal, in terms of the rights and interests of with-profits policyholders and the potential for conflict between them and the mutual. The FCA has outlined its view of the legal position but is clear that this will not be the view of all mutuals. It expects the independent expert appointed by the mutual to seek independent legal advice so that they can understand all points of view. The firm, independent expert and the FCA are all expected to have an interest in the appointment of an appropriate legal adviser.

The recommendation of legal advice is an additional cost, which was not reflected in the cost benefit analysis of the consultation paper. The paper proposed that a one-off cost of £32,000 should cover the cost of applying for the waiver. The FCA recognises that these costs may need to be increased for legal advice. There is no indication of how much of an increase is required but the consultation responses raised concern over the cost estimate being too low, before the need for legal advice.

Vote of with-profits policyholders

The policy statement removes the existing guidance that requires a vote from with-profits policyholders on any changes to the fund structure. The current guidance in COBS 20 on a policyholder vote will remain but additional guidance will be added, stating that the vote may not apply if firms apply for the modification.

Reasons for the removal of the vote include the cost of such an exercise and the possibility that a vote gives with-profits policyholders a veto over proposals. Appropriate engagement between the mutual and members is still important. Part of the independent expert’s role is to give their view of the extent of policyholder engagement.

Length of modifications

A concern with CP 12/38 was the uncertainty of the period that the modification would apply. Although the FCA retains the ability to revoke a decision, it anticipates the length granted to the modification will be appropriate to the run-off of remaining with-profits business within the fund. It confirmed that both the PRA and FCA will grant the modification for the same length of time.

Suitability of the proposal

All mutuals should consider if the issues are applicable to them and if something needs to be done.

If they decide that they are not applicable i.e. a waiver of the rules is not relevant, it is important to be able to demonstrate this and if necessary, share this with the regulator.

If the issues are applicable, applying for a waiver may be suitable. The statements highlight other options available to mutuals with declining with-profits business, including going through legal proceedings to separate the fund or using product innovation as a means of increasing business.

As mentioned, with-profits mutuals that are writing sizeable amounts of with-profits business can also apply for the waiver. However, they would be required to show that current rules are burdensome. They will have to decide whether now is the correct time to apply and, if so, the evidence they can provide for the waiver to be approved.

What should mutuals applying for a waiver be doing?

-

Mutuals are required to provide evidence of the principles and in particular be able to demonstrate the continued appropriateness of the modification to their business plan. This could take considerable time and effort.

-

The statements recognise the difficulty in deciding the interests of different policyholders. Mutuals are required to appoint an independent expert, who, in turn, is advised seek legal advice.

-

Although a policyholder vote is no longer required, communication remains important. This is likely to include notification to members and accounting for any objections.

-

Approval of the modification is required by both regulators. The PRA has confirmed that any application should be made to the FCA in the first instance, which will then co-ordinate with the PRA. Any waiver will be issued jointly.

Further information

You can read the FCA statement here and the PRA statement here.